Sunday, October 31, 2010

Saturday, October 30, 2010

Thursday, October 28, 2010

Wednesday, October 27, 2010

Monday, October 25, 2010

Sunday, October 24, 2010

Saturday, October 23, 2010

DXZ Flash Crash Detonates Entire Currency Complex

And now, for that Friday night bomb, when nuking stocks has a tad too much of a Waddell and Reed 'amateur hour' aftertaste, the only alternative - destroy the entire

currency market. If this crash in the DXY (seen below) had happened during regular hours, apparently driven not by the dollar but by DXY component EUR (there was no comparable move in other USD pairs), it would have created a complete market collapse. Luckily it happened an hour after close. Weekend collapse averted. And a quick glance at the other pairs shows that the GBP and CHF were solidly impacted as well.

FIND OUT MORE

Friday, October 22, 2010

SPX and NYMO Divergence

SPX new high but NYMO is clearly in red. I have a similar setup called NYMO Sell that uses the same principle, see the top left corner in the chart below, the setup has 65% winning rate (since 2002) while the gain loss ratio is 5.2 which is astonishingly high and which means the setup is very effective in catching an exact top.

FIND OUT MORE

FIND OUT MORE

Thursday, October 21, 2010

Tuesday, October 19, 2010

Banking Index to watch

You are likely to hear a lot of noise this week about the mortgage-title problem. Normally, I would say that this shouldn't be a problem as it will get resolved.

However ... attorneys are getting into the act, and Washington politicians may jump in this week as well.

Why? Because there is an election coming up, and that could send many politicians into the mortgage-title scramble looking for votes and to be heard ... and they could create an enormous problem if they interfere.

One would expect that this would create pressure on financial institutions, so today we will look at the Banking Index chart today.

As you can see on today's chart, the index broke below a support line on Friday. But, at the same time, its Ultimate Oscillator hit an oversold level at label 6. So that may keep it in check for the next couple of days. On the upside, the Banking Index has issues to contend with such as its formidable resistance at 49.28.

Bottom line for this week: There could be a downside danger this week on the Banking Index if Washington decides to make the mortgage-title problem an election issue. If they do, then keep an eye on the 42.71 support level. If it is violated, then the Banking Index could fall to test its 41.43 support. If that should happen and fail to hold, then the likelihood is that the financial sector will be in big trouble and that would put a hurt on the market's rally.

http://www.stocktiming.com/Monday-DailyMarketUpdate.htm

Monday, October 18, 2010

Insider Selling To Buying Update: 2,019 To 1

Two weeks ago, insiders sold "only" 1,169 times more than they bought. Alas, last week selling apparently is the new black again, with selling outpacing buying on the S&P by a factor of 2,018. Insiders in Oracle, GameStop, Google, CSX and General Mills appear to be particularly partial to the new black. Something tells us CNBC will not pick up this particular piece of news.

FIND OUT MORE

Sunday, October 17, 2010

Friday, October 15, 2010

Institutional Selling Action ???

Institutional Selling Action from Stocktiming. It looks more and more like the April case as institutions selling keeps increasing despite the market keeps having higher high, so bulls still need to be careful.

FIND OUT MORE

Federal Reserve Balance Shit!

This week we have official confirmation of our speculation from last week, that the Fed is now the second largest UST holder institution after China, with $821.2 billion in Treasurys. And courtesy of yesterday's POMO schedule announcement, according to which the Fed will purchase $32 billion in UST through November 8, at which point it was have $853 billion, we now know that Brian Sack will be the biggest holder of US Treasurys in the world (surpassing China's $847 billion). Aside from this there was little notable in the weekly balance sheet update: bank reserves increased by $29 billion in the past week, as Primary Dealers added even more to their purchasing capacity post the end of quarter window dressing.

FIND OUT MORE

Thursday, October 14, 2010

As The World Markets Turn

The NYSE World Leaders Index takes the NYSE U.S. 100 and NYSE International 100 Indexes and combines them to form a global index of 200 stocks. With 100 of the NYSE's largest U.S. company listings and 100 of its largest foreign company listings, the NYSE World Leaders Index has a float-adjusted market cap of $13.5 trillion. This represents 68% of the market cap of all stocks listed on the NYSE. Currently this index is trading at key long term horizontal resistance and just below its 50 Month and 200 Week EMAs after recently breaking its downtrend from the 2007 high.

If this index is able to sustain its recent breakout and move above the 200 Week EMA then a significant rally is likely to ensue. A month or so later we would then be looking for a 50/200 long term bull cross to confirm the move. It's unlikely that such a rally would occur absent an expansion in world GDP. And this is what the chart appears to be forecasting at this time. On the other hand, a failure of the breakout and a move back below the 50 Week EMA would call such a scenario into doubt. The next few weeks should give us our answer.

FIND OUT MORE

If this index is able to sustain its recent breakout and move above the 200 Week EMA then a significant rally is likely to ensue. A month or so later we would then be looking for a 50/200 long term bull cross to confirm the move. It's unlikely that such a rally would occur absent an expansion in world GDP. And this is what the chart appears to be forecasting at this time. On the other hand, a failure of the breakout and a move back below the 50 Week EMA would call such a scenario into doubt. The next few weeks should give us our answer.

FIND OUT MORE

Wednesday, October 13, 2010

Tuesday, October 12, 2010

I know, inevitably we’ll see some reports saying the dramatic drop of VIX today was due to some other factors. Well, the statistics below is from sentimentrader for VIX last Friday’s readings, it says according to the history, a very low VIX is not very friendly to bulls. So it seems to me whether the VIX drop today is for other factors or not, doesn’t matter because VIX was already low enough to be considered as not so bull friendly.

FIND OUT MORE

Monday, October 11, 2010

Insider Selling To Buying Update: 1,169 To 1

In this week's update of "insiders selling to idiots", we find that the ratio of shares sold-to-bought by insiders is once again in the four digit range: 1,169 to 1 to be specific. In the past week, insider buying in S&P 500 companies amounted to only $286,000, the bulk of which was in MEMC (WFR). As for the selling: well, it appears ORCL insiders just can't wait to dump as much as they can, as fast as possible.

For those who believe last week's data is an outlier, here is the weekly selling to buying ratio over the past month:

•October 8: 1,169-1

•October 1: 2,341-1

•September 24: 1,411-1

•September 17: 290-1

•September 10: 650-1

FIND OUT MORE

Sunday, October 10, 2010

Saturday, October 9, 2010

Friday, October 8, 2010

M2 Update: 12th Consecutive Weekly Increase, The Seasonal Adjustment Inflection Point, And The FDIC's "Free Capital Transfer" Plan Is Working

M2 continues its seemingly endless rise higher...at least on a seasonal adjusted basis. In the week ended September 27, M2 rose to a fresh record of $8,741.9 trillion: a$30.9 billion W/W jump which was the 4th largest weekly rise year to date. This was the 12th sequential increase in M2, which in 2010 has increased by over quarter of a trillion dollars.

We are not sure what the real reason for the surge in "real" money is (and not magically seasonally adjusted money) in Q4 is, when the NSA "deficit" catches up with the SA numbers, but whatever it is: liquidations, pick up of spending into the holidays, etc., we think "this time may be different." Which means that the next several weeks will be very critical to confirm if the actual priced in surge in NSA M2 will actually occur. And since this is real money that goes into the economy for a variety of GDP boosting endeavors, this may serve as yet another accrued source of weakness. Because should not only the $125 billion in NSA monetary aggregates (that already are priced in by the government), but an additional pick up into EOY not occur, then the impact to GDP, from a monetary basis, may be quite severe, and amount to as much as 1% of GDP. We will keep a close eye on this differential and confirm or deny whether this hypothesis is playing out.

FIND OUT MORE

We are not sure what the real reason for the surge in "real" money is (and not magically seasonally adjusted money) in Q4 is, when the NSA "deficit" catches up with the SA numbers, but whatever it is: liquidations, pick up of spending into the holidays, etc., we think "this time may be different." Which means that the next several weeks will be very critical to confirm if the actual priced in surge in NSA M2 will actually occur. And since this is real money that goes into the economy for a variety of GDP boosting endeavors, this may serve as yet another accrued source of weakness. Because should not only the $125 billion in NSA monetary aggregates (that already are priced in by the government), but an additional pick up into EOY not occur, then the impact to GDP, from a monetary basis, may be quite severe, and amount to as much as 1% of GDP. We will keep a close eye on this differential and confirm or deny whether this hypothesis is playing out.

FIND OUT MORE

Thursday, October 7, 2010

Karl Denninger Explains Foreclosure-Gate On The Ratigan Show

Visit msnbc.com for breaking news, world news, and news about the economy

Wednesday, October 6, 2010

22nd Weekly Outflow From Mutual Funds Contradicts Earlier Statement From Bob Pisani

It is not at all surprising that ICI's latest weekly flow report confirms what everyone with half a brain has known for a long time: the 22nd weekly outflow from domestic mutual funds is now in the history books. One more month, and we will have had an unprecedented 6 months of consecutive outflows, even as the market continues to levitate ever more incredulously on nothing but Fed POMO action (and Brian Sack's much more stealthy "collaboration" with Citadel), vacuum tube upward feedback-loop momentum on no volume, and the custodian banks' terrorist forced buy-in action in ETFs like SPY and IWM. Absent these three factors stocks would have been around 50% lower. In the meantime, and contrary to what CNBC was misrepresenting on national TV, the 22 weeks of consecutive outflows now amount to $76 billion in capital taken out by retail investors from domestic stock funds, and $75 billion YTD. And here is the scariest statistic for the administration, the Fed, and bankers around the world: in September $20 billion was pulled out from domestic stocks. This occured despite the nearly 9% surge in stocks. Which means that the bankers, the HFTs, the Fed, and whoever else may be accumulating stocks in expectation of retail jumping in for the latest round of passing the hot potato, is out of luck. With the failure of this latest attempt to sucker retail "dumb" money into stocks, cannibalization time for the big boys has finally arrived. Have fun passing the steaming bucket of explosive feces to each other, boys.

FIND OUT MORE

Yen Now Back To Pre-Intervention Levels

FIND OUT MORE

Agri-Food Thoughts

Munching sound in back ground is that of locusts as they make Australia their Spring snack. Australia is in the process of preparing for war against the worst locust swarms in 75 years. In September, rains began to expose massive egg beds to the warming sun, encouraging them to hatch ahead of schedule. ABC News reported,

"The Australian Plague Locust Commission says egg beds up to nearly 20 kilometres long have been exposed in north-western Victoria after the recent flooding.(10 Sep 2010)"

More recently bloomberg.com reported,

"Surveys in the Bourke, Walgett and Brewarrina regions had spotted more than 700 locust bands stretching up to 1.5 kilometers in length, Industry & Investment NSW said.(1 Oct 2010)"

While the locusts may spare most of Australia's crops, dry weather in Russia may not be so benevolent to Russian wheat. Russia announced last week that the embargo on grain exports was being extended to July of 2011. Russian government does not believe it will have sufficient information on status of Russian grain crops and reserves before that time. Rather than helping to feed the world, Russia may have to import grains to feed livestock herds.

Global reserves of Agri-Food grains are not as comfortable as some contend. The world cannot tolerate crop failures like that occurring in Russia on a regular basis. It may perhaps be able to tolerate one failure, but probably not two in one year. In coming years, could we find ourselves bidding with China, and then India, for global Agri-Food commodities in a far more competitive manner?

For investors, Agri-Food offers a rare opportunity to participate in the price inelastic portion of a long-run supply curve. The what? Agri-Food sector, on a global basis, is now operating in that sector of the long-run supply curve where prices go up more than demand. Percentage change in price is greater than the percentage change in demand, and demand is rising.

FIND OUT MORE

"The Australian Plague Locust Commission says egg beds up to nearly 20 kilometres long have been exposed in north-western Victoria after the recent flooding.(10 Sep 2010)"

More recently bloomberg.com reported,

"Surveys in the Bourke, Walgett and Brewarrina regions had spotted more than 700 locust bands stretching up to 1.5 kilometers in length, Industry & Investment NSW said.(1 Oct 2010)"

While the locusts may spare most of Australia's crops, dry weather in Russia may not be so benevolent to Russian wheat. Russia announced last week that the embargo on grain exports was being extended to July of 2011. Russian government does not believe it will have sufficient information on status of Russian grain crops and reserves before that time. Rather than helping to feed the world, Russia may have to import grains to feed livestock herds.

Global reserves of Agri-Food grains are not as comfortable as some contend. The world cannot tolerate crop failures like that occurring in Russia on a regular basis. It may perhaps be able to tolerate one failure, but probably not two in one year. In coming years, could we find ourselves bidding with China, and then India, for global Agri-Food commodities in a far more competitive manner?

For investors, Agri-Food offers a rare opportunity to participate in the price inelastic portion of a long-run supply curve. The what? Agri-Food sector, on a global basis, is now operating in that sector of the long-run supply curve where prices go up more than demand. Percentage change in price is greater than the percentage change in demand, and demand is rising.

FIND OUT MORE

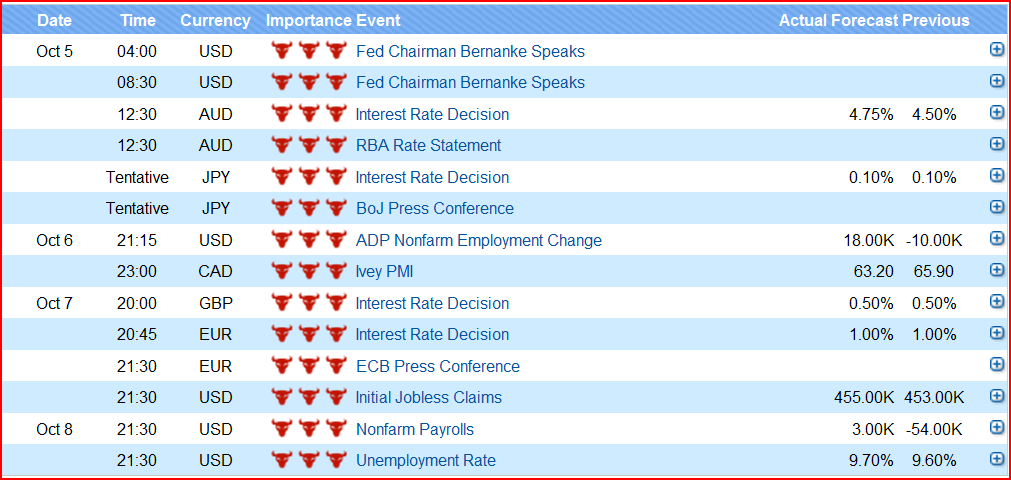

Tuesday, October 5, 2010

Sunday, October 3, 2010

Saturday, October 2, 2010

Is Europe Getting Ahead Of Itself As Excess Cash In Euro Banking System Drops To Post-Lehman Low

Find Out More

Marc Faber's October Outlook

Dollar and Currencies--The dollar is extremely oversold and investor sentiment is very bearish. Conversely, investors are very bullish on the Euro (96% bullish according to DSI). Faber believes that a inflection point could be at hand leading to a nice move upward move in the dollar. He would not be short the dollar right now.

Find Out More

Buy Rare Earth

Two rare-earth projects are scheduled to ramp up production by the end of 2012 -- one owned by Molycorp Inc (MCP) in California and another by Lynas Corp (LYC) in Australia. (Long Term Trade)

Subscribe to:

Comments (Atom)